Rental payments starting to show up in credit reports, possibly helping would-be homeowners

This can help build a good credit rating, but you must pay on time

The rent may be too damned high and until now, there hasn’t been much incentive for consumers to pay their rent on time every time. That’s changing as a number of services are making it easier to share your good payment record with lenders. That can make it easier for younger consumers to build a strong credit record that can help them qualify for a less expensive mortgage.

It’s not automatic, though, and it’s still a bit of a patchwork so it’s important to stay up to date on who is doing what to and for renters.

- The three major bureaus — Experian, Equifax, and TransUnion — can include rent payments on credit reports, according to NerdWallet.

- But they only do so if someone sends them the data — typically a landlord, property manager, or a third-party “rent reporting” service.

How it works in practice

There are three main ways rent is getting added to credit reports now:

1) Landlord/property manager programs (growing)

- Many large apartment operators now report rent automatically or offer opt-in programs.

Some states and cities are even pushing this (for example, laws requiring landlords to offer reporting options).

2) Third-party services (most common path)

- Companies like rent-reporting apps/services track your payments and send them to bureaus.

- Some only report on-time payments, others report everything (including late payments) — which can hurt you.

3) Credit-building tools tied to accounts

- Some newer fintech tools connect to your bank account and identify rent payments automatically, then report them.

Important caveat

Most rent is still NOT reported by default.

Not all services report to all three bureaus, so the impact can vary.

Not all credit scores use rent data:

Some newer models (like certain FICO and VantageScore versions) do

Many mortgage/auto lending models still ignore it, Chase cautions.

Why this matters

- On-time rent reporting can help people with thin or no credit build a score.

- But it cuts both ways: late payments can damage your credit if they’re reported.

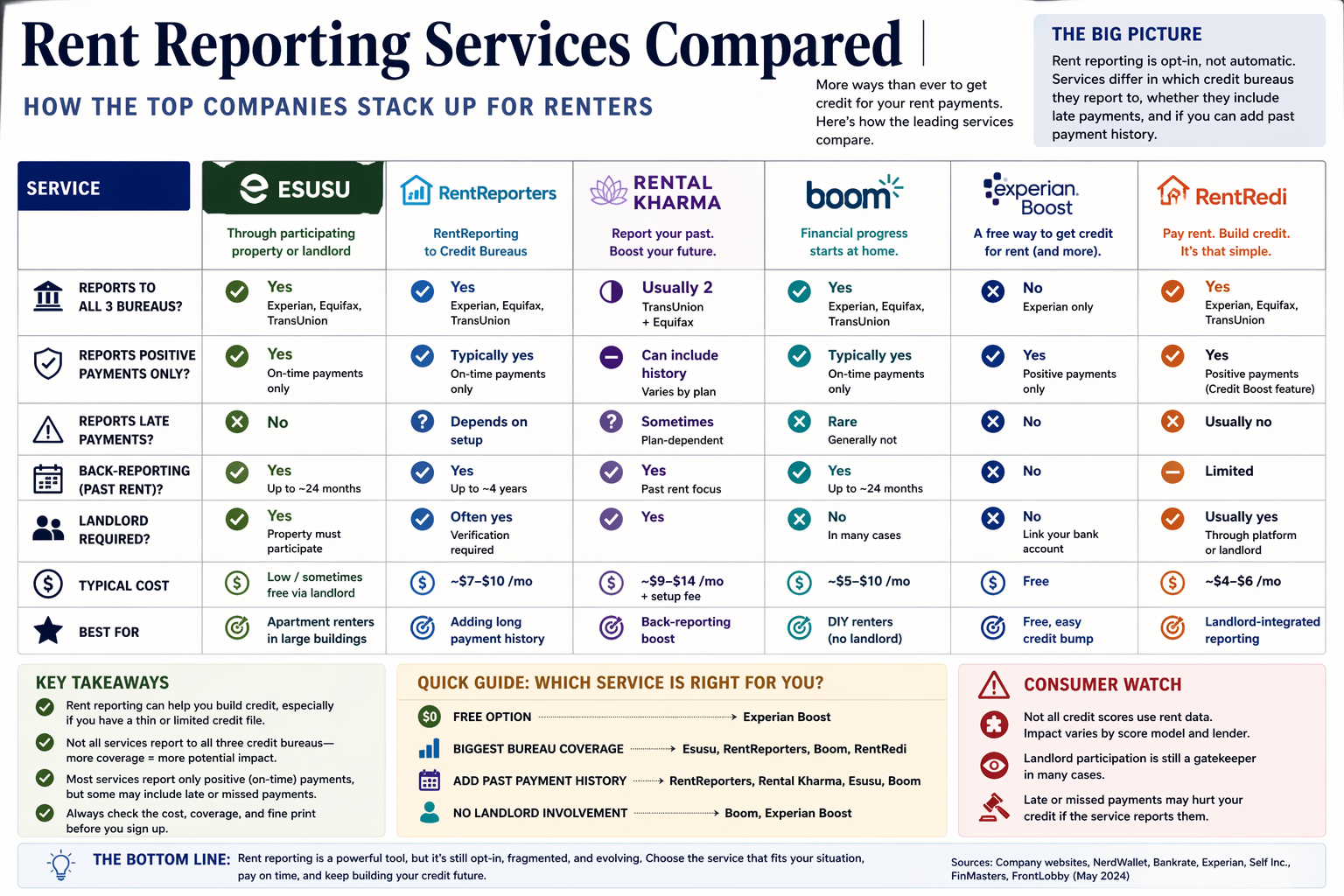

The key players in rent reporting

1) Direct-to-consumer apps (you sign up yourself)

These are the fastest-growing — and most relevant for consumers.

Experian Boost

Lets you add rent (and utilities) by linking your bank account

Reports only to Experian

Often free

Big limitation: doesn’t reach all bureaus

Self

Reports rent + utilities to all three bureaus in some plans

Designed for people building or rebuilding credit, says Firstcard

Kikoff

Lightweight credit-building service that can include rent reporting

Typically app-based, low-cost, according to WalletHub

These are the easiest entry point — no landlord cooperation needed in many cases.

2) Standalone rent-reporting services (the core industry)

These companies specialize in taking rent payments and pushing them to credit bureaus.

RentReporters

Reports to all three bureaus

Can add past rent history (a big differentiator), reports TurboTenant

Rental Kharma

Focus on back-reporting (historical rent)

Often used by people trying to boost scores quickly

Boom

Can report without landlord involvement

Reports to all three bureaus, according to Rent Reporting Center.

RentTrack

Often integrated with payment systems

Can report to all three bureaus in some setups, says AxcessRent

These are the “plumbing” of the system — they connect renters/landlords to credit bureaus.

3) Landlord / property-manager platforms (quiet but powerful)

You may be enrolled automatically if your building uses one of these.

Esusu

One of the biggest multifamily housing partners

Reports to all three bureaus, Esusu says

RealPage

Offers opt-in rent reporting subscriptions in many apartment complexes, according to RealPage.

Avail

Automatically reports rent (often to TransUnion) through its system, according to Rent Reporting Center.

This is where scale is happening — large apartment portfolios adding reporting by default or opt-in.

4) Hybrid fintech / rent-payment apps

These blur the line between payments and credit-building.

- PayYourRent

- RentRedi

- CreditClimb

These platforms:

- Process rent payments

- Then automatically report them to one or more bureaus

The key differences

Not all services are equal:

Coverage

- Some report to all three bureaus (best impact)

- Others report to only one or two

What gets reported

- Some report only positive payments

- Others report late/missed payments too (riskier)

Cost

- Free (Experian Boost) → subscription ($5–$10/month typical)

Back-reporting

- Some can add up to 24 months of past rent

- Others only report going forward

Bottom line for consumers

This is a rapidly expanding ecosystem, not a standardized system

A handful of companies — especially Esusu, RentReporters, and Experian Boost — are shaping the market

But your actual experience depends heavily on:

Your landlord

Which bureaus get the data

Whether negative payments are included

Caution required

This isn’t set in stone. It’s an evolving system and it’s changing rapidly, as landlords, lenders and the credit bureaus themselves exert pressure on the tracking services. It’s important to pay attention to details and to keep up with changes in the system.

And don’t forget to pay the rent on time.