Crowd tries to buy Spirit out of bankruptcy — but airline history suggests a steep climb

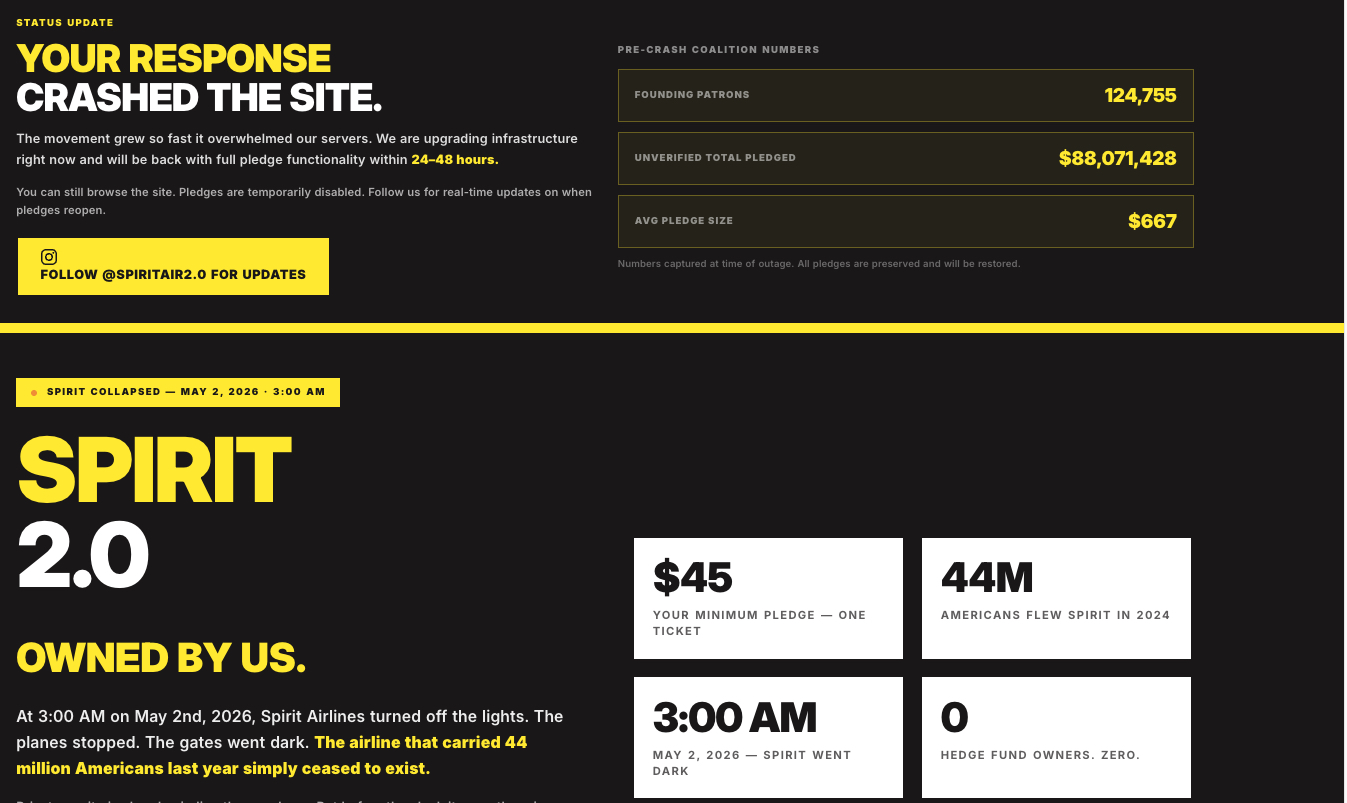

A grassroots campaign is trying to crowdfund a consumer-owned “Spirit 2.0” airline after the carrier’s sudden collapse

What’s happening - and what’s not

After Spirit Airlines abruptly shut down on May 2, 2026, a viral campaign — “Let’s Buy Spirit” — is pitching a radical idea:

Turn the failed airline into a crowd-owned cooperative, funded by small contributions from travelers.

The pitch taps into a real gap in the market. Spirit was the largest ultra-low-cost carrier in the U.S., and its disappearance removes a key source of cheap fares — especially on leisure routes.

But the airline didn’t just stumble — it collapsed after years of losses, two bankruptcies, failed mergers, and a last-ditch bailout that never materialized.

The bigger picture: airline bankruptcies are common — shutdowns are not

U.S. aviation has a long history of bankruptcy, but most airlines don’t disappear — they restructure or merge.

Major examples:

- United Airlines — Chapter 11 (2002–2006), emerged stronger

- Delta Air Lines — Chapter 11 (2005–2007), restructured and expanded

- US Airways — two bankruptcies before merging with American

- Trans World Airlines — bankruptcy led to acquisition by American Airlines

Even in recent years:

- Regional carriers like Ravn Alaska and others have filed and disappeared or been absorbed. Donald Trump “saved” the Eastern Shuttle in 1989 but it ceased operations in 1992 and was eventually absorbed by USAir.

👉 The key takeaway:

Bankruptcy is normal. Total liquidation — what just happened to Spirit — is rare

When airlines fail, billionaires — not crowds — usually step in

Historically, airline rescues have required deep-pocketed investors, not small contributors.

Examples of billionaire/major-capital interventions:

Richard Branson

Built Virgin Atlantic with substantial private backing

Later relied on government-backed rescue financing during crises

David Neeleman

Founded or backed multiple airlines including JetBlue and Breeze Airways

Carl Icahn

Took stakes in distressed airlines in past cycles, pushing restructurings

Private equity and hedge funds

Routinely provide debtor-in-possession (DIP) financing during bankruptcies

Often end up owning the reorganized airline

Even Spirit itself explored traditional rescue paths:

- merger attempts with Frontier and JetBlue (blocked)

- a proposed government-backed bailout that collapsed (Reuters)

👉 In other words:

Airlines typically require hundreds of millions to billions in capital, not grassroots pledges.

Why the “buy Spirit” idea is so difficult

1) Scale problem

Spirit once had:

- 100+ aircraft

- tens of thousands of employees

- billions in debt obligations

Even a stripped-down restart would require massive capital and regulatory approval.

2) Asset competition

Other airlines are already positioned to scoop up:

- planes

- airport slots

- routes

3) Regulatory barriers

- FAA certification

- DOT approvals

- bankruptcy court oversight

4) Timing

Spirit is already liquidating quickly to repay creditors, not holding a long auction process

Affordability Watch: What consumers lose if Spirit stays gone

Spirit’s impact went beyond its own passengers.

Its ultra-low fares forced competitors to match prices

Without it, fares are already rising on some routes

Fewer low-cost options =

higher baseline ticket prices

fewer “budget” travel opportunities

Translation: Even travelers who never flew Spirit may soon pay more.

Could a consumer-owned airline actually work?

There are precedents for fan-owned or cooperative models (like the Green Bay Packers), but none in modern U.S. aviation at scale.

To succeed, a “Spirit 2.0” would need:

- institutional investors (not just small donors)

- experienced airline leadership

- regulatory approval and operating certificates

- a radically different cost structure

What this means

The crowd-buy movement reflects something real:

Consumers want cheaper flights — and fewer dominant carriers.

But airline history is blunt:

Airlines are capital-intensive, heavily regulated, and brutally competitive.

That’s why past bankruptcies have been resolved by:

- mergers

- hedge funds

- billionaires

—not the crowd.

Bottom line

The “Let’s Buy Spirit” campaign is a fascinating test of consumer power — and a sign of frustration with rising travel costs.

But if history is any guide, the most likely outcome is still the traditional one:

👉 Spirit’s pieces get sold off — and the industry consolidates further.

Translation: Don’t put any money in the Spirit 2.0 dream. It will go the way of all dreams. Away.

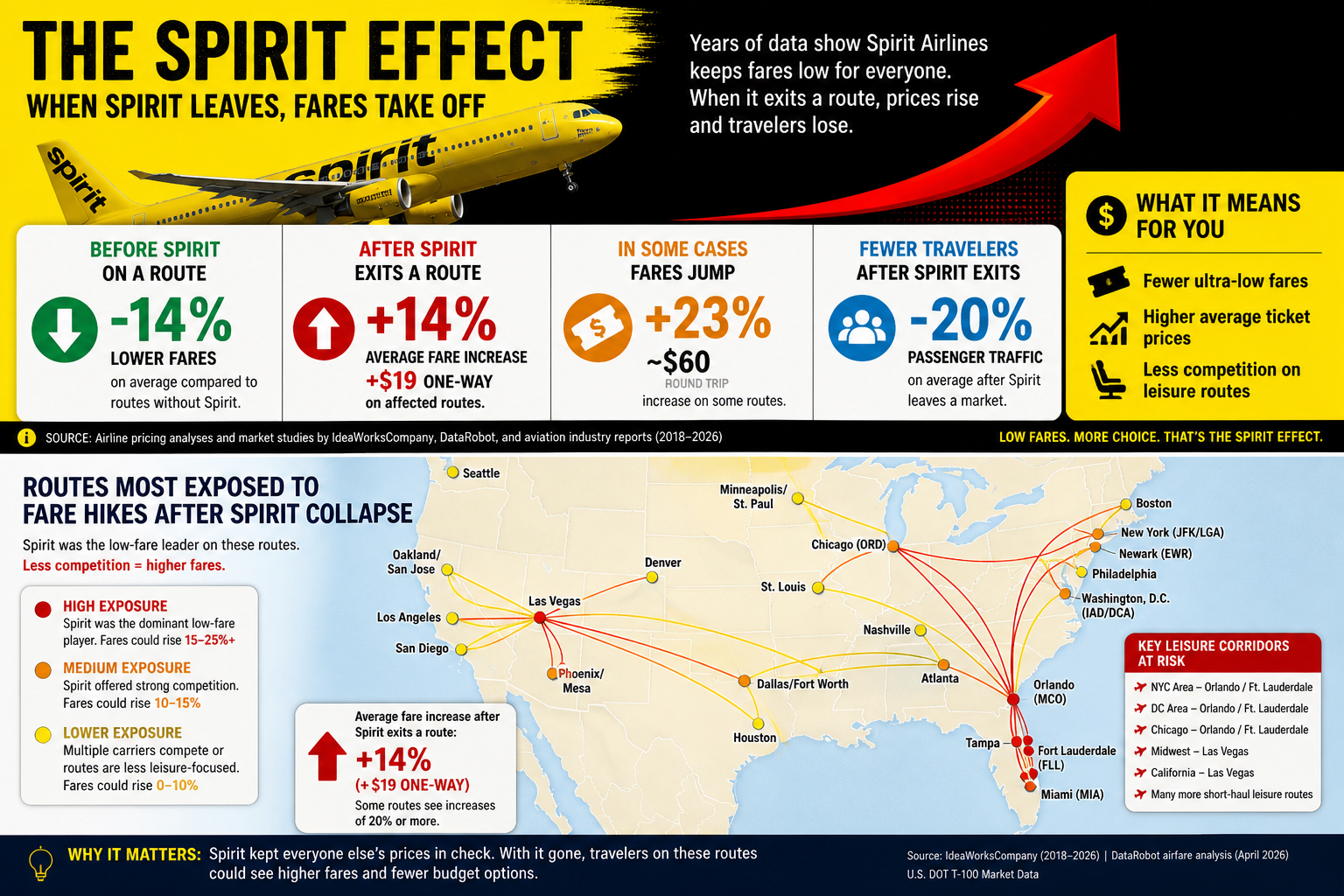

Data Box: The “Spirit effect” on airfares

Before Spirit exits a route (typical impact):

- Fares run ~14% lower on routes where Spirit operates, according to FOX 13 Tampa Bay

- Ultra-low fares often act as a price ceiling, forcing legacy airlines to match or discount, WRAL News reports

After Spirit exits (historical data):

- Average fares rise ~14% (+$19 one-way) on affected routes, said Business Insider

- In some cases, fares jump 23% (+~$60 round trip), CBS News found

- Passenger traffic can fall ~20% after exit

Extreme route examples (post-exit spikes):

- Some routes have seen fares double or more after Spirit leaves, per Business Insider

What’s happening right now (post-shutdown signals)

- Airlines are already gaining pricing power after Spirit’s collapse

- Fares are rising heading into summer travel season

- Experts warn some routes could see 15–20% increases without a low-cost competitor